The Asset Class Discovery Problem: Why the Next $14T Market Requires a New Real Estate Playbook

In the real estate industry, the most significant value creation hasn’t come from managing legacy sectors, but rather from the platforms that identified and institutionalized emerging asset classes before they became the market standard.

For a Chief Investment Officer, the most consequential question today isn’t about cap rates or interest rates. It is a question of strategic evolution: Where do new asset classes come from?

History provides a clear map for the CIO. Ten years ago, Single-Family Rental (SFR) was a fragmented, unproven category. There was no standardized underwriting for the cash flows of 30,000 individually-titled homes. By 2020, it was a $60B+ market and a permanent, financeable staple in the global real estate playbook.

The same arc unfolded with cold storage, self-storage, student housing, and data centers. Each started as a “specialized” curiosity and ended as a core asset class. The industry’s winners were the leaders who understood the demand early, built the underwriting framework before there was a standard one, and deployed capital while the rest of the market was still waiting for “comparable transactions.”

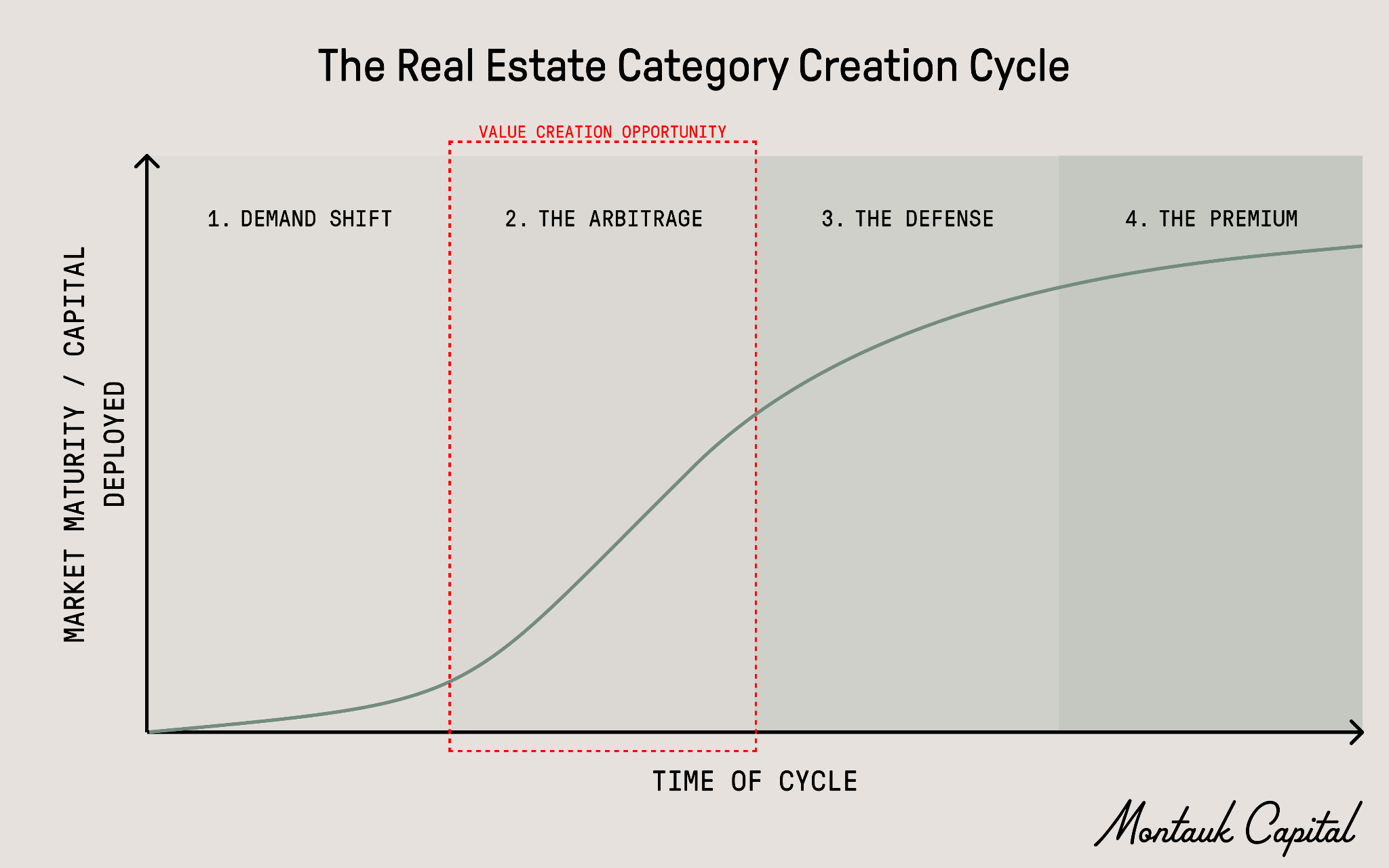

The Pattern of Category Creation

So far, we have seen that major real estate cycles have taken a four-phase path forward:

Demand Shift: A fundamental change in society (like the rise of AI or cold storage of pharmaceuticals) transforms a category of previously overlooked physical assets into essential ones.

The Arbitrage: A small group of operators figures out how to underwrite the specialized risks and the new operating model for these new assets.

The Defense: Institutional-scale capital matures the model, turning a “frontier” idea into a stable, financeable asset class.

The Premium: The broader market enters the space only after “comps” are established, ultimately paying a premium for the safety of a proven category.

From a CIO’s perspective, getting in early in this path of category creation, particularly between Phases 2 and 3, presents substantial opportunity for alpha and value creation. As such, understanding the insights underlying these transformations at the earliest stages allow CIOs to move earlier into the cycle, even as most platforms continue to enter at the end of these cycles.

Why This Cycle is Different: The Convergence of Power, Data, and Land

We are currently entering what may be the largest asset class expansion in the history of the built world: Infra Tech. This is a $14 trillion convergence driven by three forces that are reshaping the fundamental economics of the real estate portfolio:

The AI Compute Surge: AI workloads require a level of power and cooling density that traditional approaches to designing buildings were never designed to absorb.

The Power Bottleneck: The centralized grid cannot deliver the load growth that modern technology requires. New generation must now be built on-site or “behind-the-meter.”

The Decentralization of Infrastructure: Infrastructure that used to live miles away such as power, cooling, and water are now migrating into the building itself.

This shift is turning the industry upside down. The building, in addition to housing tenants, is now also housing the infrastructure that powers the modern economy, creating a massive opportunity for real estate owners and operators.

From Infra 1.0 to Infra 2.0: The Programmable Building

While Infra 1.0, the “legacy” form of real estate infrastructure focused on the “space for rent” concept where value was driven by location and square footage, Infra 2.0 turns each building into a revenue-generating platform in its own right. Rooftops become sites for power generation, electrical rooms serve as potential storage, and spare square footage on commercial floors can house edge compute hardware.

These new layers enhance the traditional real estate concept by producing contracted, indexed cash flow that flows directly into the Net Operating Income (NOI) of the asset.

At Montauk, we are already seeing this model in action through our portfolio company platforms like GridFree AI, which develops off-grid energy solutions for data centers, and Perimeter Compute, which activates existing building footprints as AI inference nodes.

Bridging the Structural Gap

Real estate companies already own the land, the permits, and the site control necessary to lead this category. However, capturing alpha in this space requires a specialized technical lens to bridge the gap between a traditional building and a high-yield infrastructure asset.

The gap exists here due to the traditional real estate market’s reliance on historical comps, vs. the need now for future-forward engineering and contracted utility to fully take advantage of technology-driven infrastructure.

At Montauk Capital, we work to help real estate platforms bridge this gap via our work as a tech-enabled infrastructure investor that can provide the technical blueprints and institutional-grade underwriting for the “New Real Estate” stack and help our partners move from Phase 4 observers to Phase 2 first-movers.

The Cycle’s Invitation

The real estate leaders of the next decade will be those who recognize that power and data connectivity have become the primary drivers of asset yield. The market is projected to grow from $14 trillion today to $27 trillion by 2035.

The gap between the assets that exist today and the assets that must exist by 2030 presents a highly compelling value creation driver for players willing to build the underwriting framework for the next category before the rest of the market gives it a name.

Matt Bisgyer is Principal at Montauk Capital.