Why Wait for Nuclear? One Solution Is Under Our Feet

TL;DR: Geothermal is the Power Solution You’re Overlooking

Geothermal is no longer a niche technology only applicable to regions near known natural geysers and specialized geologies. We are currently at the “shale revolution” moment for geothermal — transforming a restricted resource into a scalable, engineering-driven powerhouse.

The Massive Demand: With hyperscalers projected to spend over $600B this year on data centers, the market is desperate for firm, 24/7 power that intermittent wind and solar simply cannot provide.

The 5,500 GW Reality: Using “enhanced geothermal systems” that leverage tech from the shale revolution, we estimate there is enough geothermal power under the U.S. alone to power the entire country four times over.

The Fracking Advantage: We are taking the same rigs, crews, and tech that made America energy independent through the shale revolution and pointing them at heat instead of oil. It’s the same proven toolchain, just clean.

800%+ Capacity Price Spikes: Without more firm power, the grid is currently at a breaking point, evidenced by recent price surges in capacity and resource adequacy markets from California to PJM. Grid planning models indicate that geothermal is one of the key technologies to keep the lights on for AI without threatening an affordability crisis.

All the Power of Nuclear, None of the Drama: Nuclear has been trapped in a cycle of decades-long delays, radioactive waste headaches, and high costs before the first watt is even generated. Geothermal delivers the same always-on reliability, but uses standard drilling rigs to get it done in months, not decades.

Why Now: Recent announcements from leading companies in the space have shown drilling times have plummeted for geothermal wells from 70 days to just 11, and costs are projected to drop to $45/MWh by 2035 - undercutting natural gas and making nuclear look like an expensive relic.

Plug-and-Play Scalability: Unlike moonshot technologies that require years of R&D, enhanced geothermal is an engineering problem that we’ve largely solved. We don’t need to invent new fundamental science, we just need to execute and deliver.

At Montauk Capital, our investment mandate targets the twin themes of electrification and the AI era’s skyrocketing compute demands. As hyperscalers race to build data centers, with their combined CapEx expected to exceed $600B this year and power demand projected to show the strongest four-year growth since 2000, it has become undeniably clear that intermittent renewables and storage cannot carry the load alone, especially in light of key affordability pressures. To close the gap, we believe the grid needs additional affordable, firm power.

Historically, the clean baseload conversation has been dominated by nuclear. Yet, as the world waits for next-generation reactors to clear lengthy construction timelines, address lagging nuclear supply chains, and tackle waste-related hurdles, geothermal power, its less-discussed alternative, is making fast progress.

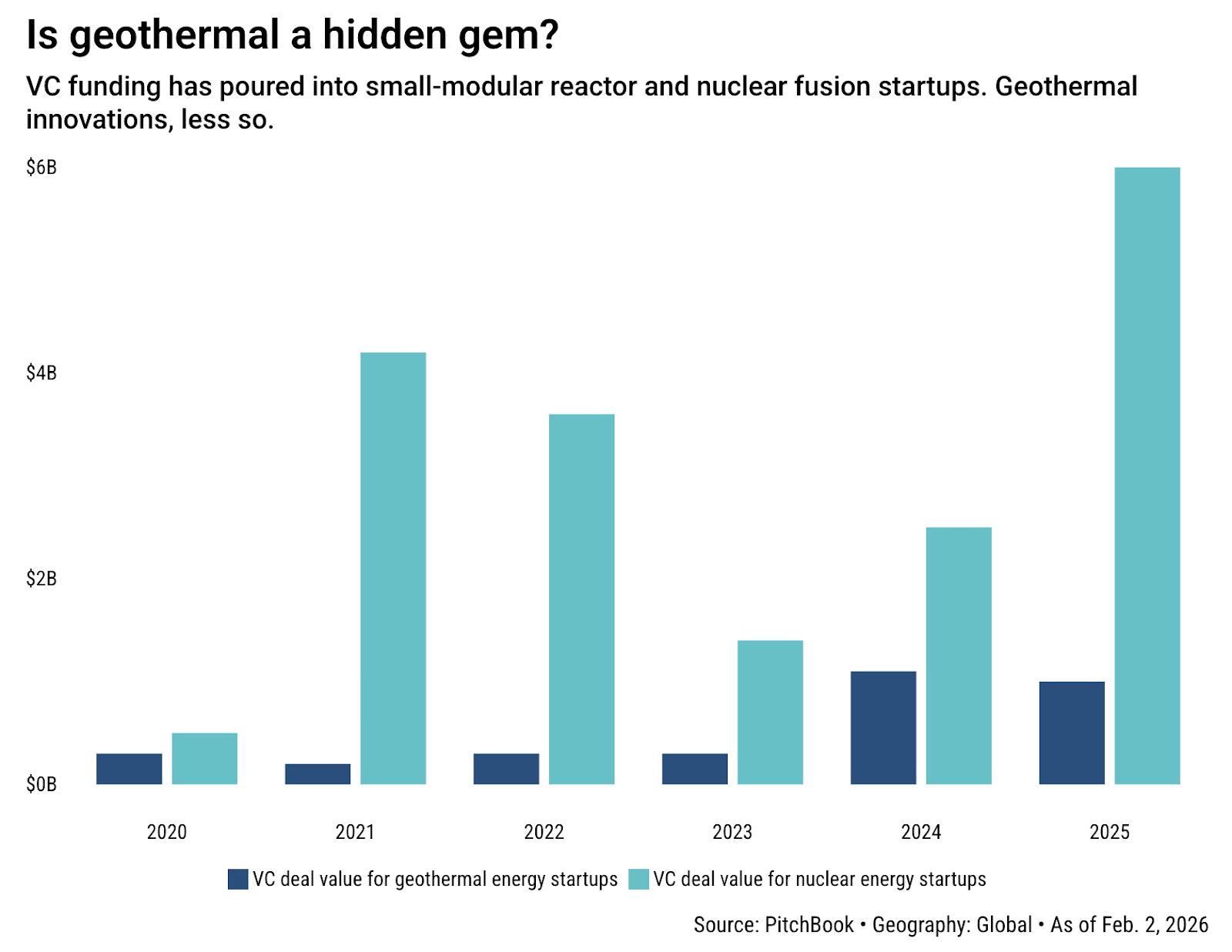

Fig 1. Global Geothermal vs. Nuclear VC Funding

Source: Pitchbook Market Insights Report

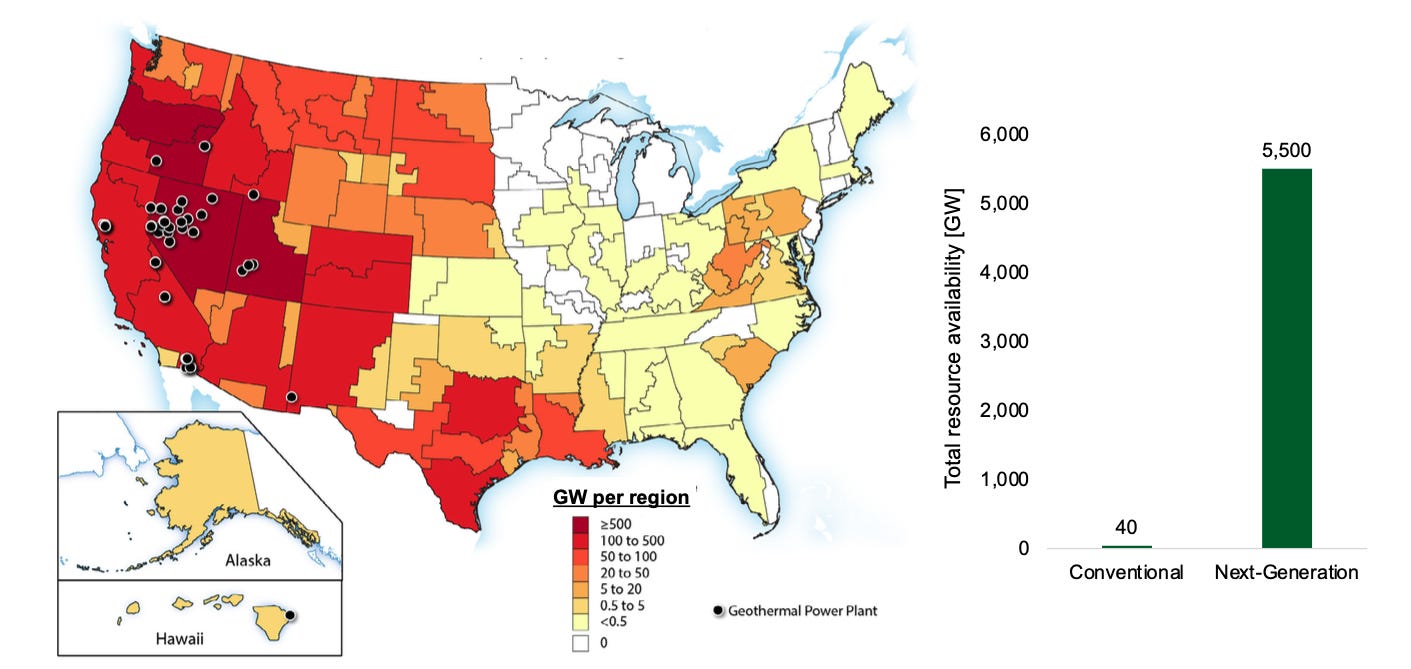

Geothermal is one of the few baseload technologies to be reducing in cost and expanding in applicability, with an estimated technical potential of ~5,500 GW underneath the U.S. alone. This capacity is equivalent to over 4 times the entire installed generating capacity of the U.S. today (1,300-1,400 GW). Yet, despite this immense potential, geothermal contributes only 0.4% of U.S. electricity generation today.

Fig 2. U.S. Geothermal: Next-Generation Potential, Current Plants, and Resource Availability

Source: DOE Next-Generation Geothermal Power Liftoff Report

For years, geothermal has been a niche resource, tethered to rare geologies like geysers and volcanoes. But that era is ending. At Montauk, we believe we are witnessing the “shale revolution” moment for geothermal, the transition from a resource-constrained asset class to a scalable, engineering-led solution.

The Grid is Under Pressure, and It’s Costing Us

The clearest signal that the market is desperate for firm power came recently from the PJM capacity market. For the energy nerds tracking the grid reliability crisis, PJM’s recent auction was a historic blowout. Capacity prices for the 2025/2026 delivery year skyrocketed by a staggering 883%. The supply crunch, driven by rapid data center growth and fossil fuel plant retirement, became so severe that for the first time, the entire market hit the FERC-approved price cap of $330/MW-day for the 2026/2027 and 2027/2028 auctions. This left PJM in a substantial reliability deficit.

For Load Serving Entities (LSEs) caught in this crunch, geothermal can be a key capacity resource. In CAISO, geothermal receives ~82% of net qualifying capacity (NQC) across all times of the day, while solar receives only ~20% of NQC due to its intermittency. By securing these capacity attributes through long-term agreements, geothermal developers can offer insulation from the capacity price spikes that now define today’s deregulated markets.

PJM isn’t alone in this capacity crunch, nor is it uniquely driving interest in geothermal. California must address price increases in its equivalent market, for resource adequacy (RA). Like PJM, California needs year‑round accredited capacity at a time when the effective load carrying capacities (ELCCs) of solar and wind in CA are projected to decline by 2030.. Over roughly the last two years, RA prices in California have risen materially, both on average and in extreme outcomes, strengthening the monetization of geothermal’s capacity value. A 2025 CPUC benchmark filing indicates system RA benchmark prices roughly doubled from mid‑teens to high‑20s $/kW‑month for jurisdictional LSEs, vs. historical 2022 RA prices mostly in the $4-15/kW‑month band. These dynamics reflect higher planning reserve margins (up to 17%), delayed new build, resource retirements, and the introduction of more granular RA requirements that stress capacity in net‑peak periods.

As RA prices climb and accreditation for variable renewables erodes, geothermal’s firm capacity becomes a more powerful driver of project economics in California. At reasonable assumptions, assuming $28/kW-month and an 85% capacity factor, geothermal’s implied capacity value is ~$45/MWh, in addition to its energy value. This will only increase as RA benchmarks continue to climb. As a result, we believe long‑term RA contracts can anchor a substantial share of a geothermal project’s revenue stack, with energy and REC revenues layered on top, making geothermal one of the few clean resources that can reliably clear RA requirements while also providing firm, low‑carbon energy.

Signed Contracts, Not PowerPoints: Geothermal Goes Hyperscale

The market is waking up to geothermal’s potential. If you haven’t been watching the geothermal wire, you might have missed a historic shift in capital over the last few months as the industry scales to meet the demand for firm generating capacity:

Fervo Energy, in January 2026, filed for an IPO, a watershed moment for the sector. This follows the company’s December 2025 announcement of a monster $462M oversubscribed Series E round led by B Capital, with new investors like Google, AllianceBernstein and others, to accelerate its Cape Station geothermal project in Utah, which itself followed a June 2025 announcement of $206M financing for the same project.

Ormat Technologies recently announced a landmark Power Purchase Agreement (PPA) for up to 150MW of geothermal energy to support Google’s data center operations in Nevada through NV Energy. This portfolio-scale agreement, enabled by NV Energy’s Clean Transition Tariff, secures a pipeline of new projects for Ormat scheduled to come online from 2028 to 2030.

Sage Geosystems closed a $97M Series B co-led by Ormat to fund its first commercial-scale project.

Zanskar recently raised a $115M Series C to expand its AI-driven prospecting platform and move into hydrothermal power plant construction.

GA Drilling just raised $44.1M led by TomEnterprise, with participation from Nabors and Underground Ventures, to accelerate the commercial deployment of its ultra-deep drilling technology.

The U.S. Department of Energy (DOE) recently announced a $171.5M funding opportunity for next-generation geothermal field-scale tests for both power generation and exploration drilling.

Not only are we seeing larger capital markets activity and some governmental support, but geothermal is also beginning to show up in real, named contracts for data centers, as hyperscalers are seeing it as one clear path to 24/7 clean power. Google’s 2024 deal with NV Energy and Fervo was the first flagship example: a “clean transition tariff” under which NV Energy will procure 115 MW of enhanced geothermal from Fervo to serve Google’s Nevada data centers, on top of an earlier 3.5 MW pilot that’s already online. More recently in January 2026, Ormat has signed a 20‑year PPA with Switch for about 13 MW from its Salt Wells plant in Nevada, its first direct contract with a data center operator and a template for pairing firm geothermal with AI and cloud campuses. In 2025, Meta and XGS agreed to develop 150 MW of advanced, closed‑loop geothermal in New Mexico, in two phases on the PNM grid, with both phases targeted to be online by 2030 to supply Meta’s local data center operations.

Behind these headline deals, developers are starting to frame multi‑hundred‑megawatt projects explicitly around AI and hyperscale demand, even if the ultimate offtakers aren’t yet disclosed. Controlled Thermal Resources and Baker Hughes have definitive agreements to advance up to 500 MW of geothermal at the Hell’s Kitchen project in California, pitched as 24/7 baseload to “fuel AI and hyperscale data centers,” with Baker Hughes supplying high‑temperature drilling and field services.

For now, public pricing is thin, but reporting around Fervo’s utility‑facing PPAs suggests a band roughly in the high‑two‑digit to low‑three‑digit $/MWh range for new firm geothermal, implying that early data‑center‑driven contracts are paying a premium over generic renewable PPAs in exchange for location, capacity value, and 24/7 carbon‑free credentials.

We’ve Cracked the Code: Geothermal Anywhere, Anytime

At Montauk, we’ve been diving into the technologies which take advantage of resource potential in light of execution challenges, unit economics, and ability to scale. Although we see clear use cases for different types of geothermal in different regions, we view Enhanced Geothermal Systems (EGS) as the key approach to fundamentally shift the global energy sector and win against other resource types.

1. Stop Looking for Geysers, Start Drilling Everywhere

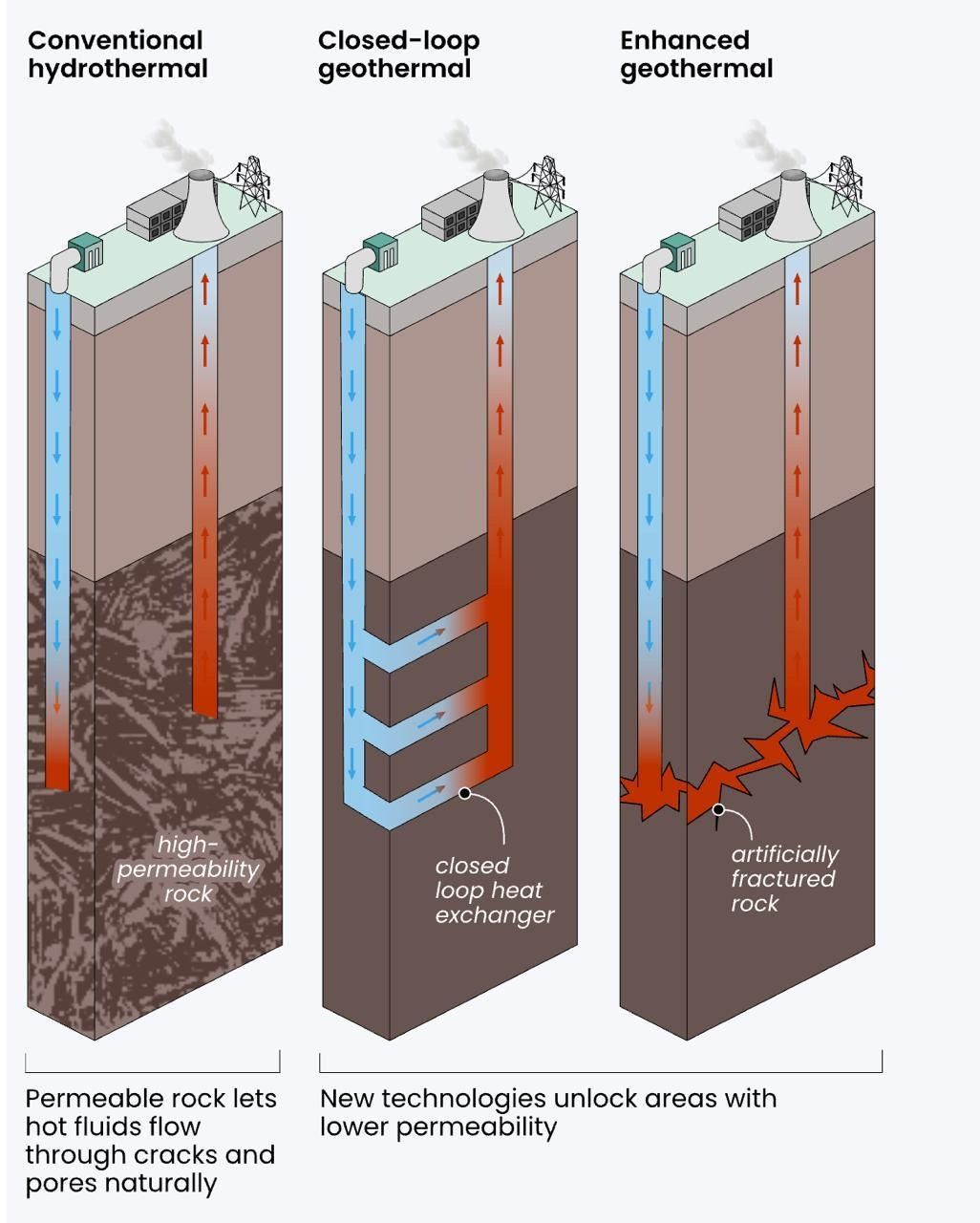

Geothermal has historically been tethered to rare tectonic regions like Iceland or the California Geysers, but EGS changes the map entirely. By fracturing hot, impermeable rock to create artificial reservoirs, as illustrated below in comparison to conventional and closed-loop (sometimes called advanced geothermal systems or AGS), EGS decouples geothermal power from the need to discover hot subsurface water, and instead allows the operator to use the earth as a radiator. It was this requirement for hot subsurface water reservoirs that had limited the scalability of the geothermal industry, and the new approach opens the market to be technically accessible across ~25% of global land area. Because it isn’t tied to specific geologic features, EGS can be deployed directly near major load centers in North America, Europe, and Asia, solving long-haul transmission bottlenecks that plague wind and solar.

Fig 3. Three Approaches to Geothermal Power Plants

Source: EMBER Heat Beneath Our Feet Report

2. A Secret Weapon to Stop Overspending on Grid Overbuilds

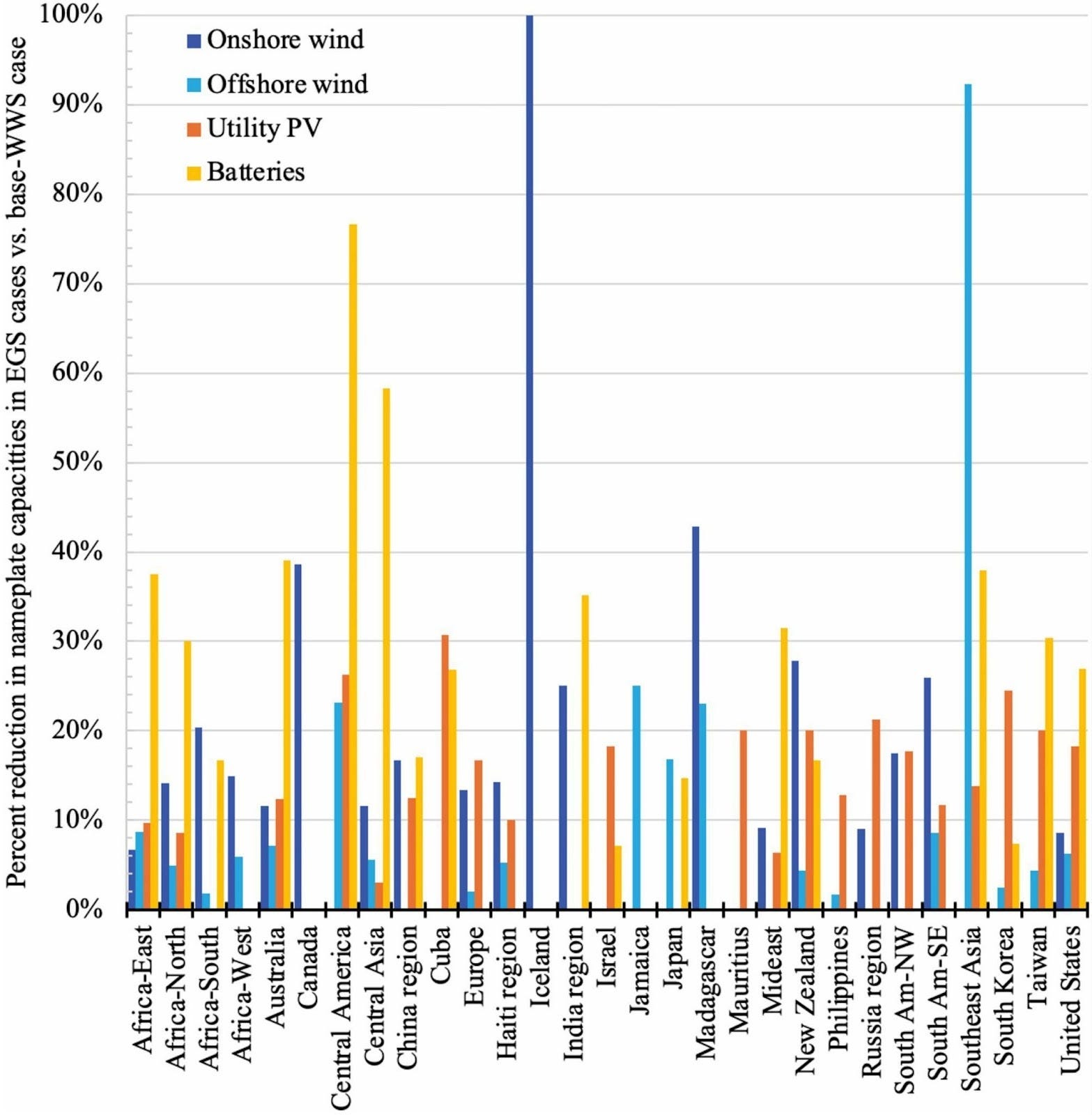

A common bear case for the energy transition is that a 100% renewable grid requires a near-infinite buildout of battery storage. EGS is the optimization lever that breaks that math. Modeling indicates that integrating just 10% EGS baseload into the mix provides a massive systemic dividend, slashing the need for nameplate battery capacity by 27.5%, with percent reductions across renewable technologies per country shown below, and reducing the total global land required for renewable infrastructure from ~0.6% to ~0.5%, all relative to the wind-water-solar (WWS) base case. For land-constrained economies with high energy density needs, like South Korea and Taiwan, EGS becomes even more attractive.

Fig 4. Reductions in Nameplate Renewables and Batteries due to EGS, by Region

Source: “Sustainability’s Impact of EGS on Transitioning All Energy Sectors Study,” Cell

3. All of Nuclear’s Promise, None of the Meltdowns (or Red Tape)

We often hear nuclear and geothermal placed in the same bucket of carbon-free, baseload power. While we get it - both offer the promise of “always-on” power and both have historically been less politically divisive - we see that grouping as a disservice to geothermal. Geothermal offers the same grid role, firm power with a high capacity factor, but without the historical cost overruns, decade-long construction timelines, or waste proliferation risks. And while nuclear has yet to see any next-generation reactors completed outside of China, South Korea, and Russia to date, Fervo, Sage, Zanskar, Mazama Energy, and other geothermal players are demonstrating real, immediate scalability with actual drilling and production progress.

To nuclear’s credit, once small modular reactors (SMRs) are operational, they will be well-positioned to service existing data center clusters, the majority of which are on the U.S. East Coast and are likely to remain concentrated to preserve the low-latency benefits of their proximity, whereas geothermal has the greatest resource availability in the western U.S. However, we see SMRs potentially coming to market in decades, not years, so as long as geothermal continues to scale and come down the cost curve at the rate it has thus far, we see it as a critical part of the supply mix for firm power required by today’s digitization.

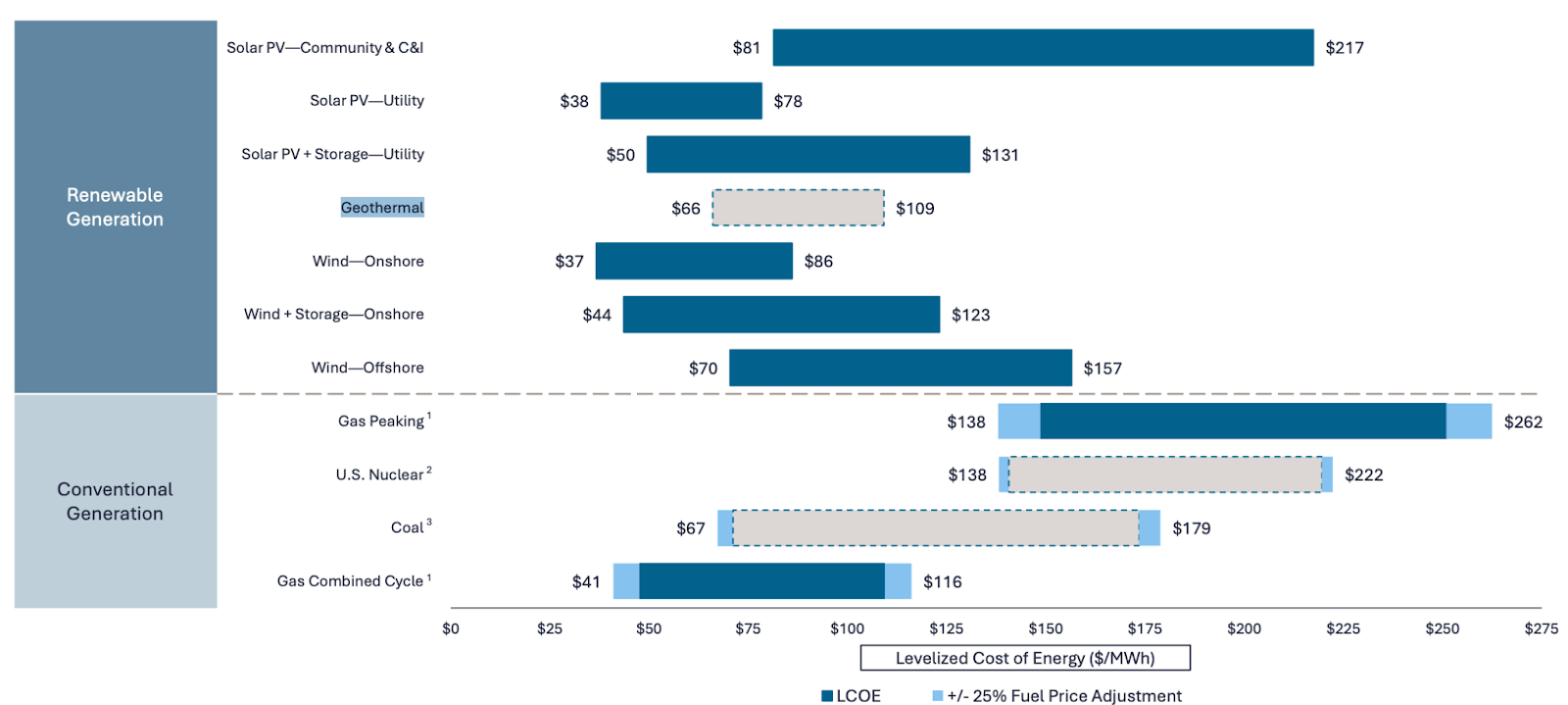

EGS also takes a direct shot at natural gas. Unlike gas-plus-storage solutions, which are subject to fuel price volatility, long lead times, and limited battery durations, EGS offers indefinite duration storage inherent to the reservoir itself. With current LCOEs of $66-109/MWh and a projected LCOE of $45/MWh by 2035, EGS is set to undercut the cost of new gas in the U.S, which sits at $41-116/MWh and climbing.

Fig 5. Lazard’s Estimated Levelized Cost of Energy by Technology Type

Source: Lazard LCOE+ Analysis, June 2025

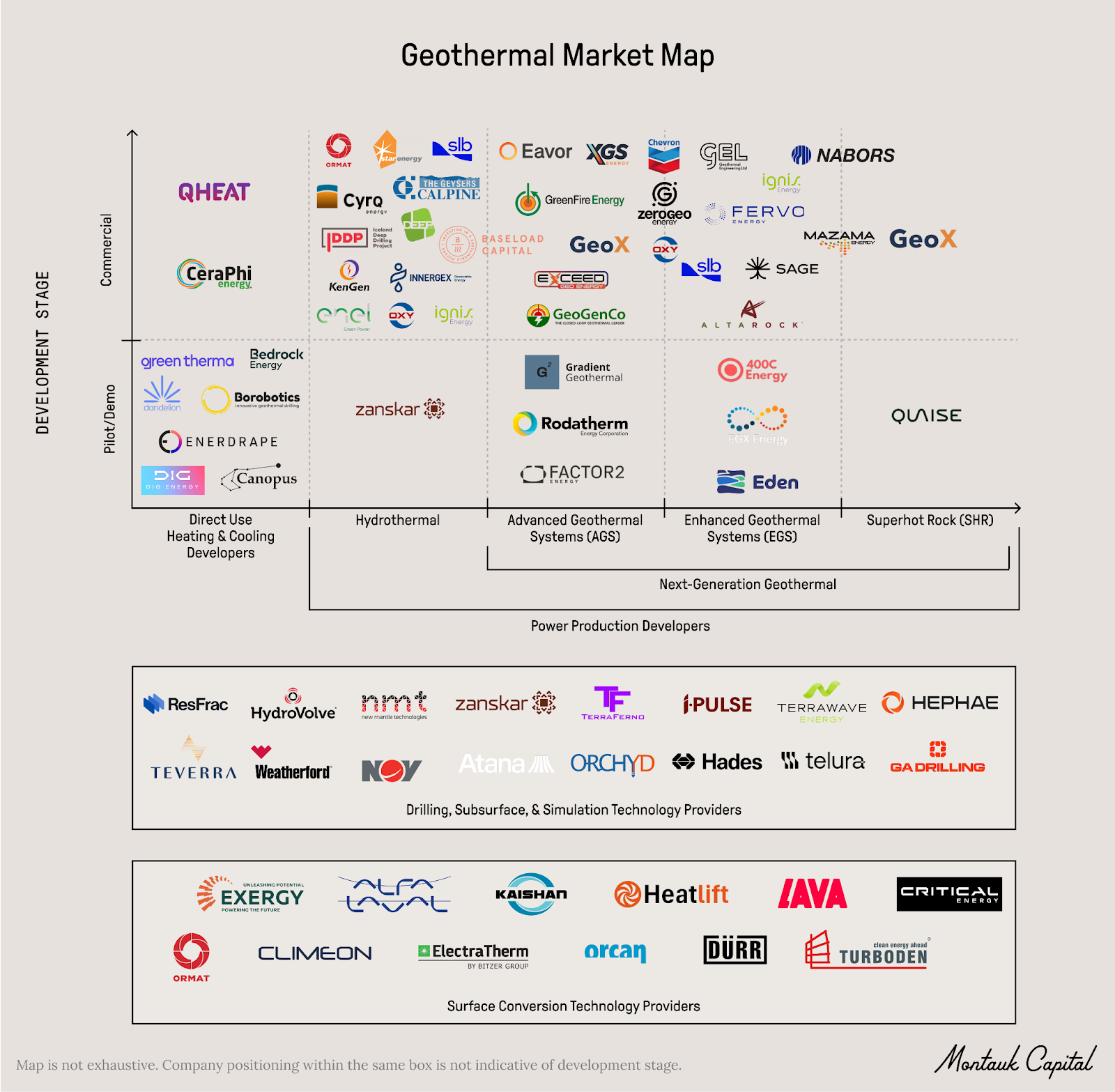

4. Market Map: The Energy Sweet Spot - 24/7 Power that Actually Scales

When you look at the geothermal tech stack, EGS sits in the “goldilocks zone” of energy density and commercial readiness.

Fig 6. Montauk Capital Geothermal Industry Market Map

Vs. Advanced Geothermal Systems (AGS) & Hybrid Closed-Loop: These startups are developing closed-loop or novel cycle architectures to generate power through conduction and reduce resource risks tied to sufficient natural water and rock permeability. Companies like Eavor are drilling separate vertical wells that connect horizontally miles underground to create a conductive, closed loop radiator, a method with technical complexity that is has taken longer than expected to scale (Eavor’s flagship project in Germany started producing 0.5MW from one loop in late 2025 vs. a planned 8.2MW from four loops). To their credit, other players including XGS Energy and Rodatherm are using single-well closed loop designs (often tube-in-tube) to minimize drilling complexity and surface footprint, with Rodatherm specifically targeting niche applications such as salt domes.

Other approaches like Factor2 Energy are developing a closed-loop system that uses supercritical CO₂ as a working fluid to drive a thermosyphon effect, aiming for higher power density than water-based systems, while Gradient Geothermal focuses on a co-production closed-loop process, retrofitting existing O&G wells with modular ORC units to generate power from waste heat. For each of these closed-loop systems, since conductive heat transfer through pipe walls is less thermodynamically efficient than the convective transfer used in EGS, AGS requires significantly more drilling to achieve the same power output, which means increased capital.

Vs. Superhot Rock (SHR): A subset of companies are targeting reservoir temperatures exceeding >350ºC, where energy density is projected to be 10x that of conventional geothermal. While achieving 5-10x energy density is a feat we’re excited for startups to begin tackling, operating at >400ºC comes with substantial material science challenges today. At such temperatures, current tools melt and electronics fry, so we view these as longer term bets that the industry will likely achieve closer to the 2040s than 2030s. To access these superhot depths beyond the economic limit of mechanical depths, several players are developing contactless drill bits to melt or vaporize rock. Quaise Energy and Terrawave are both developing millimeter-wave drill bits, but differentiate as Quaise is currently a developer, while Terrawave plans to be a technology provider. Quaise plans to transition to a technology provider as the geothermal ecosystem continues to mature. GA Drilling is similarly developing a plasma-based drill bit, but has also expanded its product offerings to include the NexTitan, which allows them to be a technology provider and innovate on their own wells today. The NexTitan is a downhole anchoring and drive system that can integrate with a standard Polycrystalline Diamond Compact (PDC) drill bit to grip the wellbore and apply extra force to the drilling assembly. I-Pulse is another technology provider that has been developing pulsed-power technology for nearly 20 years, and has recently entered the geothermal scene for contactless drilling.

A new entrant to the contactless drilling space is Hades Mining, which plans to start as a technology provider of electric impulse drilling for deep rock vaporization, with additional applications in in-situ mining applications. Another new entrant to the contactless drilling space is Telura, which is pursuing the tech from a laser drilling angle. Mazama Energy is a unique SHR player that differentiates from others by targeting SHR via EGS techniques in volcanic settings. Rather than developing novel drilling physics, Mazama focuses on high-temperature stimulation and licensing its methodologies, recently deploying flow control technologies from 400C Energy to manage reservoir performance. It’s important to note that we are increasingly seeing exciting convergence between SHR and EGS, with many EGS players accessing or starting to access temperatures >350ºC.

The EGS Sweet Spot: EGS comparatively uses hydraulic stimulation to create permeability in hot, impermeable rock, generate heat via convection, and primarily operates at temperature ranges where O&G tooling can be adapted today, allowing drillers to leverage the ~61% of the O&G workforce who pursue activities directly transferable to geothermal. As the DOE puts it in the newly launched application for next-generation geothermal field tests, “EGS is the most mature of the next-generation geothermal technologies and currently offers the greatest potential for power generation per drilled foot.” Fervo Energy leads this category, having demonstrated commercial viability via horizontal drilling with a PDC bit and fiber-optic sensing. EGX Energy is positioning itself as a fast follower, focusing on Tier 1 acreage (e.g., The Geysers) and modular 50 MW deployments. 400C Energy has so far served as a technology provider to Mazama Energy, a player pursuing SHR via EGS, as discussed in the SHR section and is developing proprietary high-temperature fracturing methods and flow control devices to manage thermal short-circuiting in EGS reservoirs, with plans to develop its own wells. Sage Geosystems is another frontrunner that uses a gravity-based fracturing approach and a “lung” mechanism, creating a two-well system that operates like a two-cylinder engine and does not require connecting an injection and production well as done in traditional EGS. By doing so, Sage can hold fractures open with pressure and reduce water losses (limiting to ~2%) relative to traditional EGS. Eden Geopower is distinguishing itself by developing electric reservoir stimulation, electric fracking, which uses high-voltage electricity to fracture rock as a potential alternative to traditional hydraulic fracturing, thus avoiding the parasitic loads and fluid circulation inefficiencies associated with pumping high-pressure water.

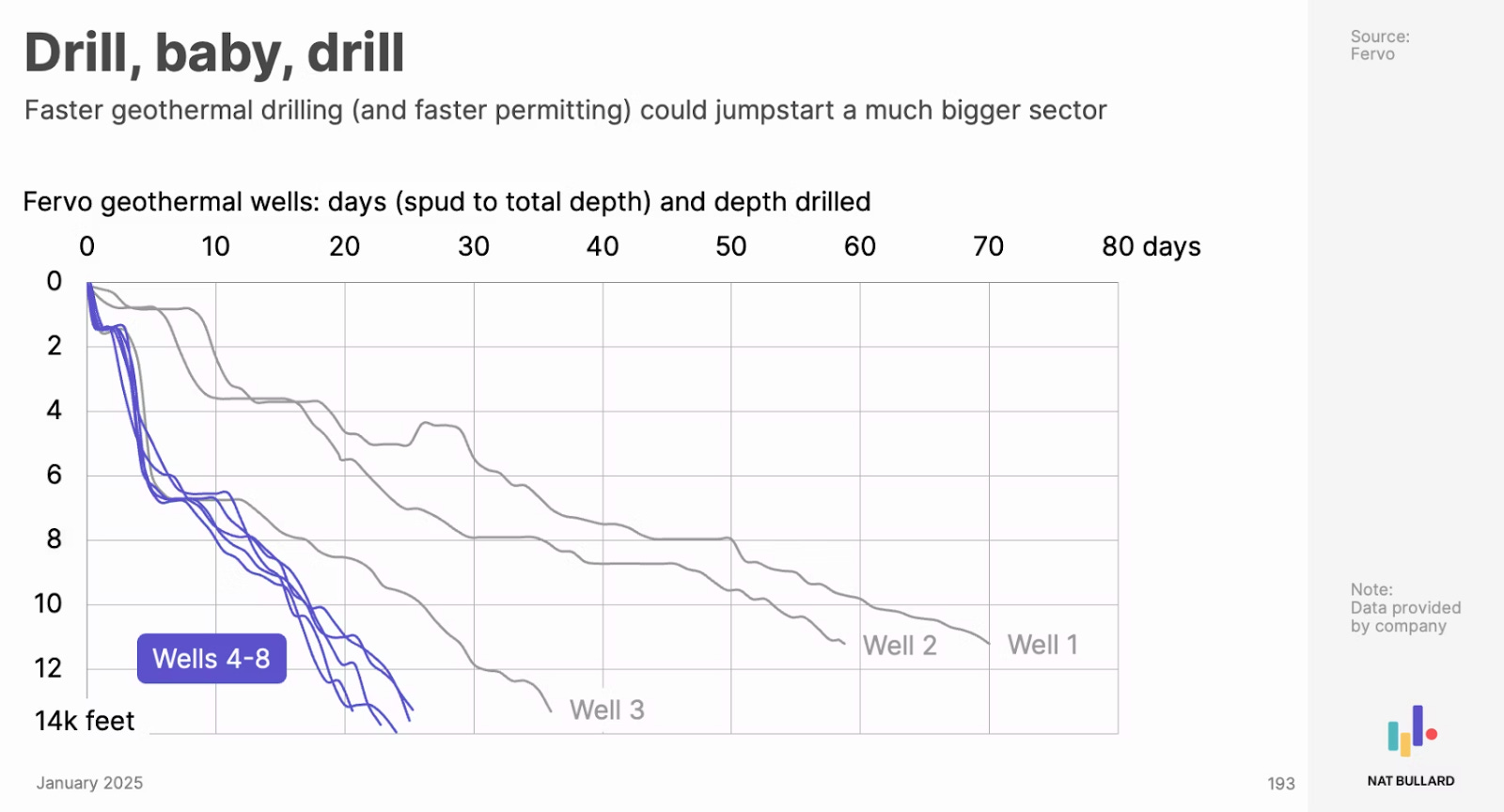

Why Wait 20 Years for a Reactor? Fervo Just Did it in 11 Days.

If the geothermal renaissance needed a definitive proof point for 2026, Fervo Energy just delivered it by drilling a well in under 11 days. At the 51st Stanford Geothermal Workshop this past week, co-founder and CTO Jack Norbeck revealed the results of their appraisal drilling campaign at “Project Blanford” in Millard County, Utah. The data confirms what we’ve been arguing at Montauk: the learning curve is real, and it is accelerating faster than the market anticipated.

Fig 7. Fervo Drilling Days vs. Depth Drilled

Source: Nat Bullard’s 2025 Annual Decarbonization Presentation

The headline numbers from Blanford represent a step-change for the industry. The vertical appraisal well reached temperatures exceeding 555°F (~291°C) at a depth of 11,200 feet, making it the hottest well in Fervo’s portfolio to date, surpassing both Project Red and Cape Station. Perhaps even more shocking than the heat was the execution, at a rate of drilling the well in <11 days, Fervo shattered their own original record of slashing drilling days for Cape Station’s wells 1 to 8 from 70 to 21 days, respectively. For an industry historically plagued by slow, expensive drilling cycles, this speed is a massive marker of improved productivity. Critically, Blanford isn’t just about heat; it’s about where that heat was found. Fervo has successfully expanded its proven geologic footprint from the hard, granite rock of its earlier projects into hot sedimentary formations, specifically sandstones, claystones, and carbonates.

Norbeck highlighted that proprietary AI-enabled subsurface analytics were central to identifying this play, validating the thesis that data-driven prospecting can drastically lower exploration risk.

While Fervo didn’t release a new explicit LCOE figure at Stanford, the physics of Blanford point directly to unit economic improvements. The Blanford appraisal demonstrates an ultra‑hot, high‑gradient, multi‑GW sedimentary resource drilled quickly, which supports higher per‑well output, more compact wellfields, and better plant efficiency, core LCOE drivers. AI‑driven exploration and faster drilling times are exactly the levers that underpin the often‑quoted ~50-70% cost reduction versus first‑of‑a‑kind EGS, even if Fervo did not put a fresh explicit $/MWh stake in the ground at Stanford.

What Keeps Us Up at Night (Besides the Heat)

All of this sounds promising for EGS, right? But what could go wrong? Let’s be realistic, although many exciting advancements have and will continue to be made across the geothermal landscape and, from our perspective, for EGS in particular, next-generation geothermal is still a nascent industry working through risks inherent to such a phase of scale-up.

Subsurface Uncertainty & Execution Risk: Even with advanced modeling, there is a risk that the resource temperature or flow rate is lower than expected once drilling occurs. If the rock is not hot enough, it cannot generate sufficient steam, and if permeability is too low, water cannot flow through the system. For example, operators like Gradient Geothermal noted instances where O&G clients attempting EGS found resources that were not flowing as expected or not as hot as projected.

Reservoir Management, Water Loss & Short-Circuiting: A major technical challenge is managing fluid flow through fractured rock. Without precise control, water follows the path of least resistance, leading to thermal short-circuiting where fluid returns to the surface without absorbing sufficient heat. Unlike the O&G industry, which uses established tools for zonal isolation, geothermal operators lack mature hardware to dynamically regulate flow across different reservoir sections. Additionally, maintaining system pressure can be difficult, with projects experiencing ~10-30% water loss to the surrounding formation.

Induced Seismicity: The process of creating reservoirs by injecting high-pressure fluids to open fractures inherently generates small seismic events. If mismanaged, particularly by interacting with pre-existing faults, this can trigger larger-scale seismicity, potentially leading to project shutdowns and community opposition. Demonstrating significant data points, Fervo recently reported zero seismic events noticeable at the surface during recent drilling.

Tool Failure at High Temperatures: Current drilling electronics and mechanical components, such as elastomers in blowout preventers and packers, often fail or degrade at temperatures >175°C. In wells ranging from 200-400°C, steel drill strings undergo significant thermal expansion, which can cause rigid connections to fail or lock up. These complications can force operators to stop drilling to cool the well (staging), while drill string degradation can compromise well integrity.

Thermal Decline: If the reservoir cools faster than projected (e.g., 5% vs. target 1% annually) due to poor heat exchange management, it can increase the LCOE and setback project economics.

The Tipping Point: From Niche Tech to New Normal

To truly understand the opportunity at hand, we need to zoom out beyond the developers and look at the market as a whole. Looking at the technology providers, we see two groups emerge: one focused on innovations to enhance drilling, completions, and simulations, while another focuses on surface conversion technologies.

Drilling, Subsurface, and Simulation: Innovators in this segment are addressing specific bottlenecks in hard-rock drilling and are selling or licensing their technologies to operators, rather than drilling themselves. Hephae creates high-temperature (200°C+) Measurement While Drilling (MWD) and Rotary Steerable Systems (RSS) designed to eliminate expensive staging time required to cool standard tools. This both speeds up existing geothermal operations and enables operators to steer wells at deeper depths without frying their tools. Terraferno is working on high-temperature completion technologies - a space which has not seen significant innovation since the shale era, but together with drilling accounts for up to 70% of total project costs. As discussed in the SHR section, players including Terrawave, GA Drilling, and Hades Mining are working on contactless drill bits, and a wellbore anchoring system in the case of GAD, that can be licensed by other operators. Other specialized providers are filling the gap between O&G software and geothermal needs. ResFrac provides industry-standard hydraulic fracturing and reservoir simulation software, acting as a critical architect for EGS design and zonal isolation strategies. Teverra combines consulting services with proprietary downhole tools for rock property measurement and workflows to assess the geothermal potential of existing hydrocarbon wells. Zanskar uses AI-driven exploration models to identify hidden geothermal resources, starting with conventional hydrothermal development, with potential to move into EGS in future years as EGS comes down the cost curve. Zanskar started as a technology provider with their agentic exploration model, and has since transitioned to developing their own wells in-house.

Surface Conversion: While drilling technology often receives the most attention, surface power conversion remains a limiting factor for project economics. Standard Organic Rankine Cycle (ORC) power plants, which are responsible for vaporizing geothermal heat to drive a turbine and produce electricity, operate at just 12-15% efficiency, capturing only a fraction of the energy produced. Current geothermal turbines are designed for lower temperatures, while fossil fuel turbines are built for much higher heat, leaving next-generation geothermal projects without an optimized off-the-shelf solution. Critical Energy is a startup modernizing the ORC design with a modular architecture, allowing operators to size capacity up or down and implement hardware upgrades as technology improves, while Lava Power is engineering specialized heat engines to optimize energy delivery. While Ormat remains the established incumbent for binary plants, serving as a design partner for pilots, Kaishan is capturing market share by leveraging high-efficiency screw expander technology to handle the complex, two-phase fluids often found in deep EGS environments.

The ranging focus areas of the technology providers point to a market opportunity. The industry doesn’t need moonshots - it needs reliability. Over the last decade, we solved for cheap intermittent electrons. Geothermal, especially EGS, has the subsurface resource, the transferable O&G toolchain, and the early proof points to play that role.

What’s missing now isn’t physics, it’s ongoing and scaled execution: standardization, bankable project models, and a deeper bench of developers and technology providers. The heat is there. The demand is there. The question is how quickly markets and policy can catch up.

Over the coming months, we’ll share more on how we’re partnering with geothermal industry leaders to further unlock this potential. If you’re excited about geothermal, come talk to us.